Why Borrowing Power Is Still a Hot Topic in 2026 And why it’s being talked about so much right now

Mortgage - Broker, Forster - Mid North Coast

As the budget draft for 2026-27 is being drawn, one of the most hotly discussed pieces is the Labor Government talk to reduce the Capital Gain Tax discount on property sales. While revenue is required for a functioning country, the effect of this proposal will impact all Australians. Property investors while in the short term will hurry to sell their properties, in the long term they will hold onto their properties longer. For developers, the higher Capital Gain Tax margin will reduce the financial viability of these new building sites. Creating a knock-on effect on housing affordability, decrease in new home construction, decrease first-time home buyers, and increased housing shortages. Renters will also certainly feel this hit! With property investors unlikely to sell, the rental prices are sure to increase. Making it even more difficult for Australians to live the dream of having their own roof over their heads. The very thing the government is trying to increase with these changes. I'd propose getting a 100% discount on CGT for investment properties sold within the next five years. This will allow more stock to come onto the market, triggering a drop in house prices. Therefore, creating greater affordability through a flood of new properties in the market and reducing property prices. #CGT #CapitalGainsTax #PropertyTax #RealEstateTax #HousingTax

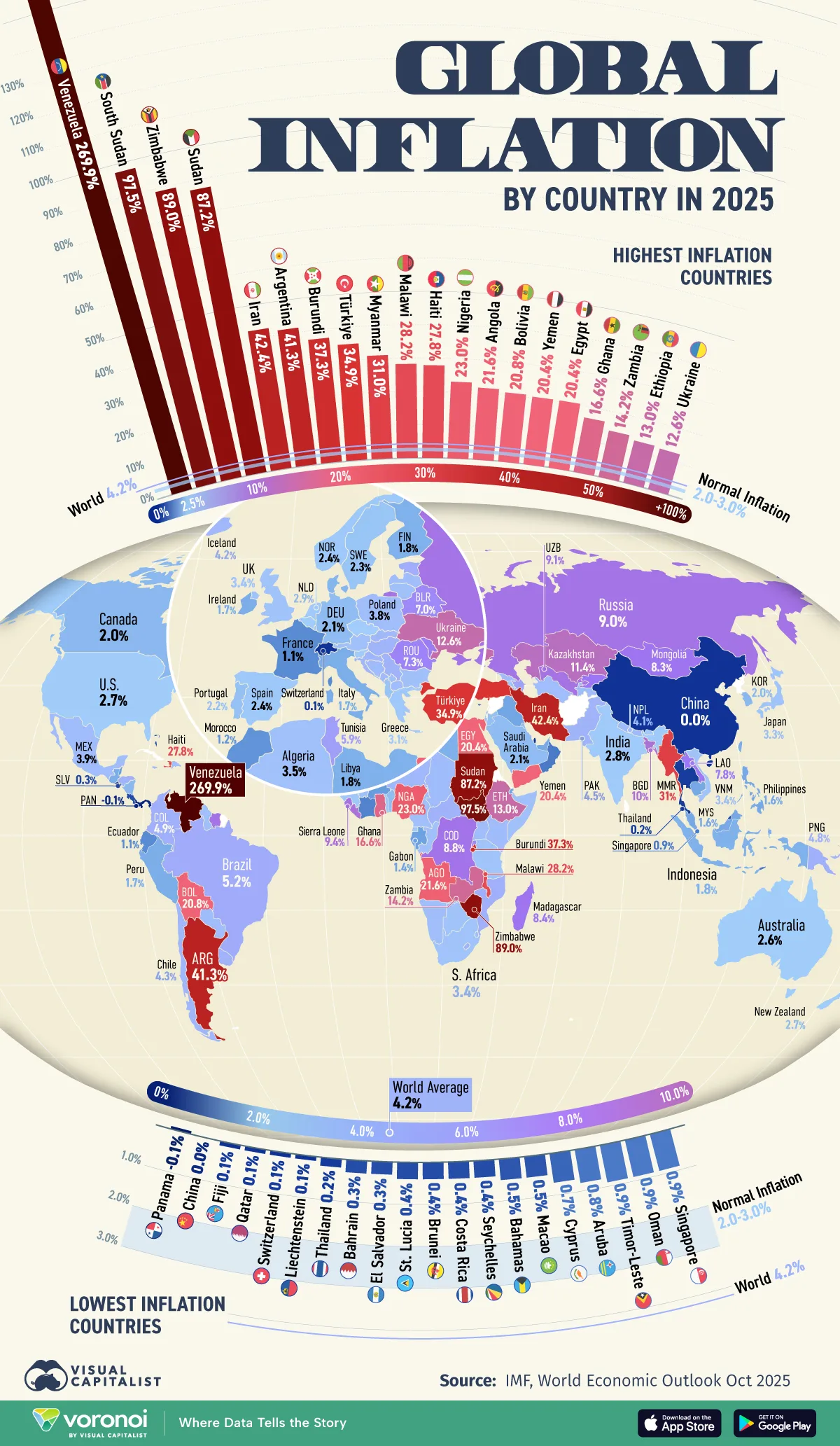

Global I nflation in 2025: What It Means for Australian Borrowers Inflation remains one of the most closely watched economic indicators in 2025, shaping central bank decisions and influencing household budgets worldwide. The latest data from the International Monetary Fund (IMF) and the Reserve Bank of Australia (RBA) paints a complex picture of global and domestic inflation trends and what they mean for mortgage holders and prospective buyers. Global Inflation Trends According to the IMF, global inflation peaked at 9.6% in September 2022 and has been on a downward trajectory since. By September 2025, the global average stood at 3.6%, with advanced economies and emerging markets both experiencing a slowdown in price growth. However, the decline is uneven: Venezuela leads with a staggering 269.9% inflation rate. Sudan, Zimbabwe, and Iran also face double-digit inflation. On the other end, China, Panama, and Switzerland report near-zero inflation. This disparity reflects differing monetary policies, geopolitical pressures, and economic resilience across regions. Australia’s Inflation Outlook Domestically, the RBA reports that both headline and underlying inflation have eased into the target range of 2–3%. As of late 2025, Australia’s inflation rate sits at 3.4%, slightly above target but significantly lower than the global average. Key drivers include: -Easing supply chain constraints -Stabilizing energy prices -Softer labour market conditions RBA Policy Response The RBA has maintained the cash rate at 3.6% throughout the second half of 2025. While inflation is moderating, the central bank remains cautious, signalling that future rate decisions will depend on: -Wage growth trends -Consumer spending resilience -Global economic risks Implications for Mortgage Holders For Australian borrowers, this environment presents both challenges and opportunities: 1. Refinancing Windows With rates stable, now may be a strategic time to refinance before any potential hikes in 2026. 2. Fixed vs. Variable Decisions Borrowers should reassess whether their current loan structure aligns with their risk tolerance and financial goals. 3. Inflation-Proofing Your Budget Even modest inflation can erode purchasing power. Reviewing household budgets and loan repayments is essential. Final Thoughts While global inflation remains volatile, Australia’s relatively stable outlook offers a degree of certainty for homeowners and buyers. Staying informed and proactive is key and working with a mortgage broker can help navigate these shifting conditions with confidence. For tailored advice or a loan health check, reach out anytime.

Understanding the Mortgage Landscape in Australia When it comes to securing a home loan in Australia, potential homeowners are often faced with the choice

Understanding the Importance of Trusted Mortgage Consultants When it comes to securing a home loan, choosing the right mortgage consultant in NSW can be cr

Understanding the Role of a Mortgage Broker When it comes to purchasing a home in NSW Midcoast region, finding the right mortgage broker can make all the d